Why flexible software solutions are indispensable for e-billing

With the mandatory introduction of e-invoicing, based on the EU-wide EN 16931 standard, companies are faced with the challenge of not only optimising their processes, but also remaining flexible in the long term. What initially appears to be a compulsory technical task reveals a key question on closer inspection: how can companies prepare for future changes without ending up in a technical dead end?

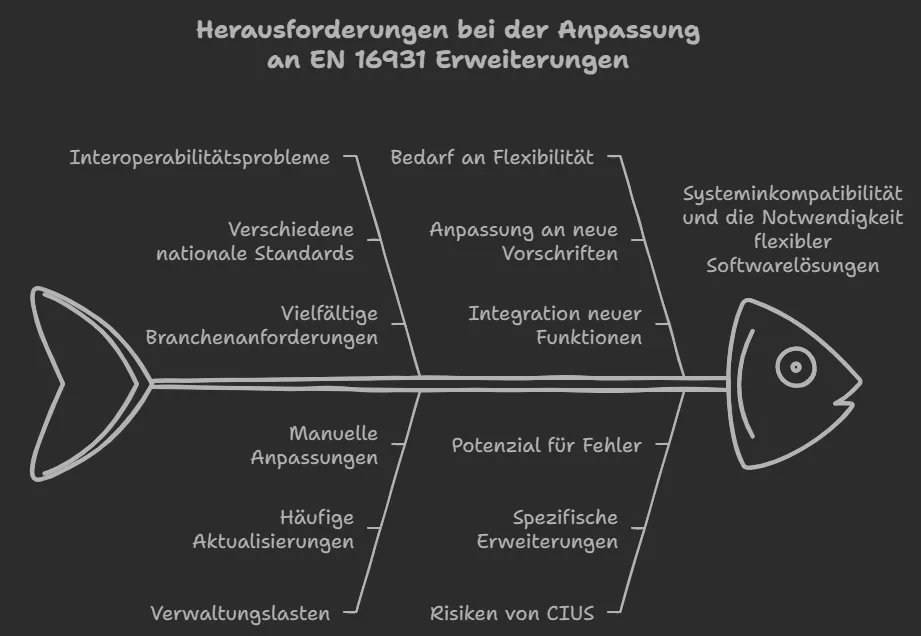

EN 16931: The standard and its limits

the EN 16931 creates a framework for the electronic exchange of invoices within the EU. The goal is clear: interoperability and efficiency. Invoices in machine-readable format, such as XML, enable automated processing. However, the standard leaves room for national and industry-specific adaptations, so-called Extensions.

These extensions can contain additional information that goes beyond the basic standard. This sounds positive at first, as individual requirements are taken into account. But this is also the crux of the matter: Not all systems are compatible. What happens if the recipient of an e-invoice cannot process the specific extensions? Companies are faced with the task of constantly adapting their systems to new standards. The challenge of extensions: CIUS and more.

A concrete example of these expansion options is the CIUS specification (Core Invoice Usage Specifications). It allows national or industry-specific requirements to be integrated into the e-invoice. However, this flexibility harbours risks. Changes or new requirements from authorities or trading partners can result in significant adjustments.

Without flexible software solutions this dynamic quickly turns into an administrative nightmare. Companies need systems that can cope with changes without extensive reprogramming.

Beware of misunderstandings

A common misconception is that EN 16931 prescribes a single, fixed file format. Instead, it defines a Semantic data modelwhich can be realised in various formats. The most common formats include UBL (Universal Business Language) and UN/CEFACT. Companies can therefore choose the format that best suits their technical circumstances.

Another misunderstanding concerns the CompatibilityIt is often assumed that all systems that support EN 16931 work together seamlessly. In reality, however, differences in technical implementation - for example in the interpretation of certain data fields - can lead to compatibility problems. It is therefore crucial to carefully harmonise the systems used.

ERP systems as a centralised solution

ERP systems form the backbone of many companies. They integrate financial accounting, warehouse management, sales and more. Changes to a single interface, such as invoice processing, can affect other modules. A practical example: A new invoicing standard could require adjustments to the finance module that have an unforeseen impact on warehouse management.

The advantage here is Expandable ERP systems such as SAP Business One. They enable companies to use integrated add-ons such as cks.onevoice flexibly or update it without jeopardising the entire system.

Outlook for the future: New requirements for EN 16931

The further development of EN 16931 will further increase the requirements for e-invoicing systems. Possible changes could include

- New mandatory fieldsAdditional information such as environmental or sustainability data could become part of the invoice.

- Extended interoperabilityImproved conversion between formats such as XInvoice and ZUGFeRD.

- SecurityStronger focus on encryption and authentication.

- Technological integrationGuidelines for blockchain or AI-supported validation.

These developments show that companies must remain flexible in order to meet future requirements.

E-Invoicing 2026: From Receipt to Mandatory Issuance — what SMEs must clarify now

E-invoicing in Europe: Harmonised standard and national fragmentation

E-invoicing in SMEs: The clock is ticking

France E-invoicing 2026: What companies with a French tax number need to know now

Service description in the e-invoice: How much detail really needs to be included?

Verifactu in Spain: the new invoicing obligation

The e-invoicing regulations in Europe

The advantages of the e-bill 2025

E-bill 2025 FAQs