From 1 September 2026, a comprehensive e-invoicing mandate will come into effect in France. This will fundamentally affect all companies based in France or holding a VAT registration there. Those who have not yet begun preparations risk missing the deadline – as the technical, organisational, and data-related requirements are considerable.

Read more: Frankreich E-Rechnung 2026: Was Unternehmen mit französischer Steuernummer jetzt wissen müssenWhat the mandate requires from September 2026

The French mandate requires all affected companies to fulfil two parallel obligations: the E-bill and the E-Reporting.

the E-bill effective from the due date, the classic paper or PDF invoice for domestic B2B transactions between companies registered for VAT in France is completely replaced. A mere PDF file is therefore no longer sufficient – a structured electronic format, transmitted via an approved platform, is required.

That E-Reporting it supplements e-invoicing where no domestic B2B e-invoice is generated: i.e. for cross-border B2B transactions and domestic B2C sales. In these cases, companies electronically transmit the tax-relevant transaction and payment data to the tax administration. The business partner can continue to receive a familiar format, however, the mandatory data additionally goes in a structured format to the state platform.

In short: e-invoicing is the electronic original document in B2B domestic transactions, and e-reporting is the purely fiscal data submission for everything beyond that.

Who is affected – and from when?

As a general rule, all entrepreneurs established or registered for VAT in France fall within the scope of this directive, including branches.

However, the introduction will be phased in:

- From 1 September 2026: Obligation to Reception from e-invoices for all company sizes. In addition, large and medium-sized companies (ETIs) are beginning with the issuance and reporting obligation.

- From 1 September 2027: Disclosure and reporting obligations for SMEs and micro-enterprises as well.

Companies without a SIREN number – such as certain financial market players or very new entities – are formally within the scope but benefit from a sanctions tolerance as long as they cannot be included in a directory listing.

The platform model: PPF, PA/PDP and OD

The mandate provides for a clearly defined platform ecosystem. Each company chooses a platform through which it sends and receives invoices and reports mandatory data to the state. There are three types of actors:

| Actor | Roll |

|---|---|

| PPF Public Billing Portal | State Platform, Directory Management, Data Hub for the DGFIP |

| Performance and Development Plan (Authorised platforms) | Accredited private platforms for the exchange and reporting of e-invoicing data |

| OD (Dematerialisation Operator) | Technical service provider without its own reporting authority, always via PPF or PA |

In practice, the chosen platform – either the PPF directly or an accredited PA – routes the invoice to the recipient platform and simultaneously reports the mandatory data to the tax authorities. ODs are responsible for the technical conversion, but are only permitted to forward tax data via the PPF or a PA.

Permitted formats and technical requirements

The mandate allows selected structured syntaxes, including:

- Factur-X (Hybrid PDF/XML format)

- UBL 2.1

- UN/CEFACT CII

A pure PDF is no longer sufficient for this. Furthermore, all companies must their SIREN or SIRET number register in the central directory (Annuaire) so that invoices can be routed correctly. Further mandatory fields include VAT IDs, tax codes, service types, and payment terms.

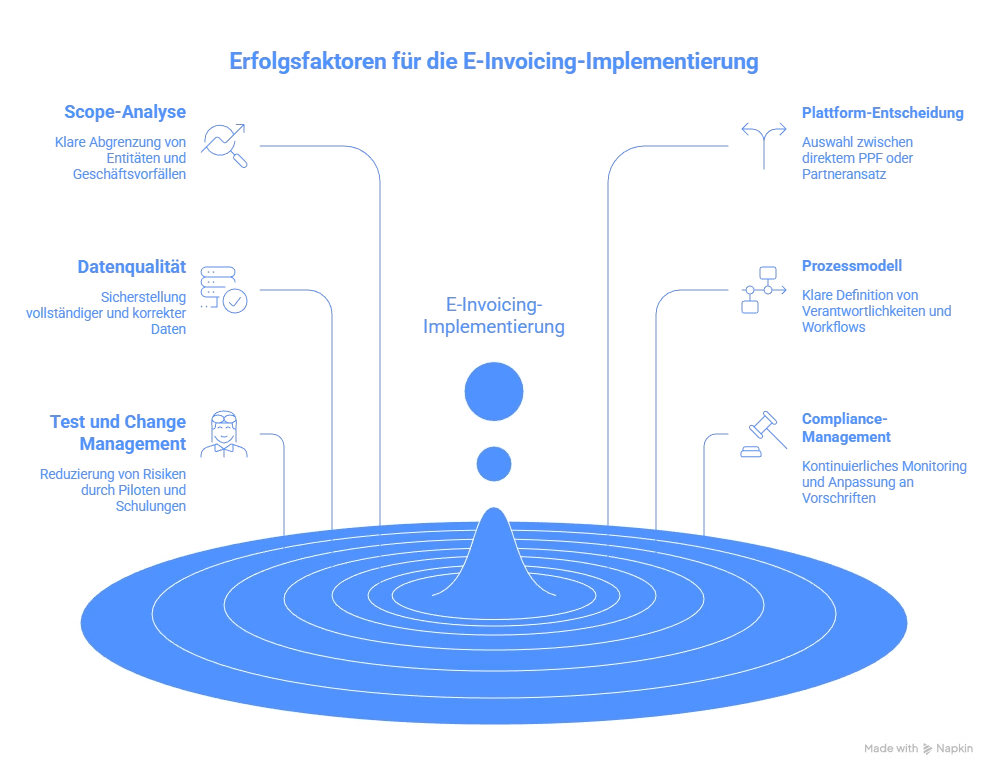

What matters in an implementation project

From the perspective of an ERP or integration project, several factors determine success or risk:

1. Scope and mandate analysis First, it is essential to clearly define which entities, branches, systems, and business transactions are in scope. Therefore, a mapping of the tax logic (Place of Supply, B2B/B2C, domestic/international) in the ERP system is recommended early on.

2. Platform and Architecture Decision Companies must decide whether to go directly via the PPF or via an accredited PA/PDP partner. Furthermore, the question arises as to whether the same provider can also cover other countries such as Italy or Poland.

3. Data and Format Quality All mandatory fields must be completed and accurate. Additionally, consistent mapping of ERP structures to Factur-X, UBL or CII is required – including line item data, discounts and references to orders or delivery notes.

4. Process and Role Model Responsibilities for invoice creation, validation, corrections (cancellations, credit notes), and status monitoring must be clearly defined. Consequently, approval, workflow, and dunning processes must also be adapted to the near real-time transparency of the tax authority.

5. Testing, Piloting and Change Management Early participation in pilots or parallel operation with real business transactions significantly reduces risk. Furthermore, Finance, Sales, Purchasing, and IT must be trained – and customers and suppliers informed about changed requirements such as the mandatory SIREN declaration.

6. Compliance and Risk Management Changes in legislation and simplification measures – such as the recent reduction in reporting scope or sanction tolerances for missing SIRENs – require continuous monitoring. Furthermore, technical and organisational measures for archiving, signatures, and failure scenarios in the event of platform downtime must be planned.

The recommended start: Design project in 4 to 6 weeks

A proven starting point is a short design project with four core components: mandate analysis, target architecture, platform pre-selection, and an end-to-end example process – from the ERP document to the Factur-X file and platform notification. This allows companies to create the necessary clarity before embarking on technical implementation.

The time until September 2026 is shorter than it appears. Those who start the analysis now will gain the leeway they need for a clean implementation.

E-Invoicing 2026: What is changing now for SMEs and SAP B1 users

E-Invoicing 2026: From Receipt to Mandatory Issuance — what SMEs must clarify now

E-invoicing in Europe: Harmonised standard and national fragmentation

E-invoicing in SMEs: The clock is ticking

France E-invoicing 2026: What companies with a French tax number need to know now

Service description in the e-invoice: How much detail really needs to be included?

Verifactu in Spain: the new invoicing obligation

The e-invoicing regulations in Europe

The advantages of the e-bill 2025