From 1 January 2025, every B2B company in Germany will have to be able to receive electronic invoices – regardless of turnover. One and a half years later, the discussion has shifted: Instead of just the legal situation, in spring the focus will be on the concrete application of e-invoicing in 2026, error avoidance, and the next stage of the dispatch obligation. Those in the medium-sized business sector who do not take corrective action now risk an IT service provider onboarding backlog from 2027 and, in the worst case, losing their ability to deduct input tax.

Read more: E-Rechnung 2026: Vom Empfang zur Versandpflicht — was der Mittelstand jetzt klären mussThree categories of error – and their consequences for input tax deduction

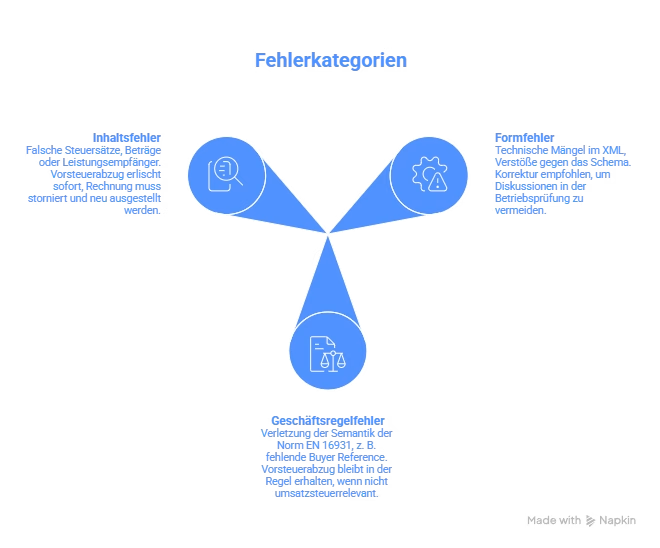

In March and April 2026, the Federal Ministry of Finance further refined its position on the BMF letter of 15 October 2025. At the centre is the question of when an error in an e-invoice jeopardises the input tax deduction. Practice now distinguishes between three categories.

Formal error

Formal errors are technical defects in XML, such as violations of the schema. As long as the invoice remains legible and the mandatory information relevant to VAT is present, the input tax deduction is not immediately at risk. Nevertheless, companies should correct formal errors because they will trigger discussions during the tax audit at the latest.

Business rule errors

Business rule errors violate the semantics of the EN 16931 standard. A typical example is the missing Buyer Reference (BT-10), which many public procurers mandatorily expect. If the error is not relevant for VAT, the input tax deduction generally remains valid according to the current interpretation. However, from a civil law perspective, the recipient may reject the invoice — and in the public sector, they do.

Content error

Content errors affect core tax data: incorrect tax rates, incorrect amounts, incorrect recipient of services. Input tax deduction is immediately forfeited here. A mere correction is not sufficient; the invoice must be cancelled and re-issued.

For accounting and IT, this tripartite division means: the initial check must no longer just ask if a PDF is readable. It must classify which of the three categories an error falls into – and react accordingly.

Validation requirement: Simply filing is no longer enough

The second shift in the debate concerns what companies must do with an incoming e-invoice. Simply filing the e-mail attachment with the XML is no longer sufficient under the current interpretation. Instead, a technical check against the EN 16931 standard is strongly recommended – in practice, through dedicated validation software.

Archiving is also being defined more concretely. At least the XML data part must be stored in compliance with GoBD; the visual PDF image part is only relevant if it contains additional tax information that is missing in the XML. Anyone storing both parts is taking the safe route, but should be aware that the XML part is the primary source.

This results in a clear requirement for incoming document processing for SAP B1 users: validate, classify, archive – and do so on a per-document basis, not on a sample basis.

SME association warns of onboarding backlog

On 15 April 2026, the Association of Small and Medium-sized Enterprises (ZGV e.V.) published a submission addressing an often underestimated bottleneck: the capacity of IT service providers. If a large part of medium-sized enterprises utilises the transition period until the end of 2026 to its full extent, the implementation and onboarding projects will converge in the fourth quarter of 2026 and early 2027.

The consequence would be a bottleneck in consulting and implementation capacities precisely at the time when the shipping obligation for companies with an annual turnover of more than 800,000 euros comes into effect. The association therefore expressly recommends not waiting until the end of the transitional period.

Practically, this means for an SME with SAP B1: Those who tackle ZUGFeRD or XRechnung dispatch only at the end of 2026 will be competing with the rest of the market for the same slots with the implementation partner.

ELSTER Viewer: Stopgap solution for micro-businesses

For companies without a dedicated ERP solution, the tax authorities have provided a free e-invoicing viewer in ELSTER in spring 2026. A report from the Cologne Tax Advisor Association on 22 April 2026 categorises the tool: it makes XML invoices readable and performs a technical check.

For micro-businesses and small partnerships (GbRs), the Viewer is a sensible starting point. For medium-sized businesses with document volumes beyond individual cases, it neither replaces validation software nor integrated processing in the ERP system. Anyone planning to use the Viewer as a long-term solution is merely postponing the actual problem.

Deadlines Overview

| Deadline | Duty | Affected |

|---|---|---|

| Since 01.01.2025 | Obligation to accept | All B2B companies, regardless of revenue |

| Until 31.12.2026 | Transition period: Paper/PDF allowed with recipient's consent | All |

| From 01.01.2027 | Mandatory e-invoicing | Companies with prior-year turnover exceeding 800,000 Euros |

| From 01.01.2028 | Mandatory e-invoicing | All businesses, including small businesses |

What the Mittelstand should do now

The obligation to receive is fulfilled – at least formally. The actual work is currently shifting to three areas: firstly, robust input validation against EN 16931, secondly, error-class-appropriate responses for incoming invoices, and thirdly, timely preparation for the shipping obligation. Those who address these three points in the coming months will avoid both tax risks and the foreseeable bottleneck at implementation partners at the end of 2026.

For SAP B1 users, the concrete next step is an inventory: which incoming channel currently receives e-invoices, what validation is running, what is the archive path for the XML part, and who in the company is responsible for classifying form versus business rule versus content errors? Only on this basis can it be decided which setup in SAP Business One should cover dispatch from 2027.

E-Invoicing 2026: What is changing now for SMEs and SAP B1 users

E-Invoicing 2026: From Receipt to Mandatory Issuance — what SMEs must clarify now

E-invoicing in Europe: Harmonised standard and national fragmentation

E-invoicing in SMEs: The clock is ticking

France E-invoicing 2026: What companies with a French tax number need to know now

Service description in the e-invoice: How much detail really needs to be included?

Verifactu in Spain: the new invoicing obligation

The e-invoicing regulations in Europe

The advantages of the e-bill 2025