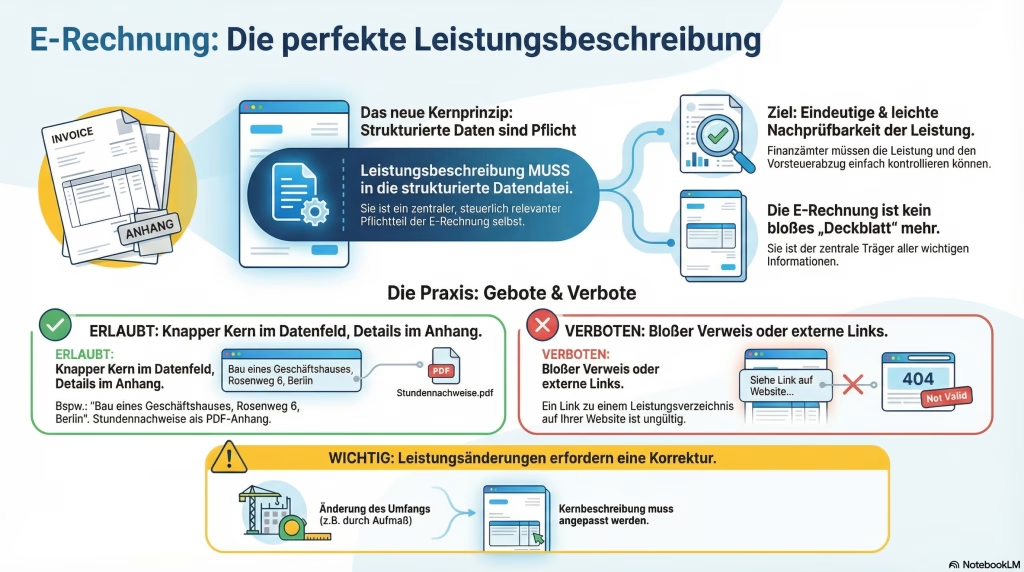

The introduction of mandatory E-bill is shifting the focus away from mere PDFs towards structured data. This is particularly noticeable in the service description: what was previously often outsourced to attachments, service specifications or delivery notes must now at least essentially be in the data file of the e-invoice itself.

{kind=link}

This article sheds light on what the Second BMF letter dated 15 October 2025 and how companies can deal with them in practice,

Read more: Leistungsbeschreibung in der E-Rechnung: Wie viel Detail muss wirklich hinein?Key Takeaways

- The service description in the e-bill must be included in the structured data and cannot just refer to attachments.

- The BMF requires a clear and easily verifiable presentation of the service in order to enable tax to be levied.

- Core information must be clear, while details are permitted in annexes, but not as a substitute.

- Changes to the scope of services require an adjustment to the service description in the e-bill or credit note.

- Companies should adapt their invoicing processes in order to fulfil the new requirements for the service description in the e-invoice.

1. legal framework: Service description as part of the mandatory information

The BMF clarifies: An e-invoice is only correct if all mandatory VAT information according to Sections 14, 14a UStG is included in the structured part of the e-invoice.

It follows directly from this:

- The service description is one of these mandatory details.

- It must be in the structured data itself.

- A mere reference to an attachment is not sufficient if the mandatory information is only contained there in an unstructured form. Otherwise, electronic processing would not be possible.

In addition, the BMF explains that Section 31 UStDV - i.e. the idea of the „invoice consisting of several documents“ - is Not applicable for e-invoices as far as the mandatory information is concerned.

This significantly changes the perspective: the e-invoice is no longer just a „cover sheet“ for collecting attachments, but the central carrier of all tax-relevant information.

2. core requirement: „Clear and easily verifiable determination of performance“

The BMF formulates a clear guideline for the service description itself:

The information in the structured part of the e-bill must contain a Clear and easily verifiable determination of performance and guarantee the control function of the invoice.

In doing so, the tax authorities are following on from the VAT Application Decree (Sections 14.5 and 15.2a UStAE). The invoice is intended to enable the tax authorities to,

- the Payment of the tax owed and

- the Right to deduct input tax to check.

The nature and scope of the service must therefore be described in such a way that this control function can be fulfilled. At the same time, the ECJ ruling „Barlis 06“ emphasises that the services provided must be not exhaustive have to be described. It is precisely in this range of tension that craft businesses now operate.

3. how concise can the service description be?

In its statement, the ZDH demanded that the service description in the structured part deliberately kept short may be used as long as it

- the performance as such,

- their scope,

- the place of performance and

- the tax rate

can be derived.

Examples are mentioned:

- „Construction of a commercial building at Rosenweg 6 in Berlin“

- „Delivery of 400 automotive spare parts“

These formulations show the target corridor: the description must be specific enough to clearly recognise the service, location and scope. At the same time, it does not have to cover every detail of individual items.

The tax authorities take up this approach in the BMF circular by emphasising the above-mentioned control function but expressly permitting supplementary information in annexes. This creates a practicable middle ground between completeness and manageability.

4. annexes as a supplement - but not as a substitute

Despite the strict requirement for mandatory disclosures, the BMF Supplementary information in annexes expressly.

For example:

- detailed timesheets,

- itemised bills of quantities or

- Further explanations

as PDF or other unstructured documents within the e-bill be attached.

However, the sequence is important:

- Key performance data (type, scope, location, tax rate) must be included in the structured part.

- details may be outsourced to the notes and then have a supplementary function.

A link to an external destination - such as a download link to a list of services - expressly fulfils the legal requirements not. Neither § 14 para. 1 sentence 3 UStG nor § 31 para. 1 UStDV consider this to be sufficient.

This means that companies must ensure that all relevant additional information actually transmitted with the e-bill and are not stored somewhere outside.

5 Practical consequences for craft and construction companies

Many projects are overflowing, especially in the skilled trades and construction industry:

- Comprehensive service specifications,

- Delivery notes with several items and

- Subsequent adjustments to quantities (measurement).

Previously, the invoice document often only referred to these documents. With the e-invoice, this procedure no longer works. Companies must therefore adapt their processes:

- the Core description of the service belongs in the structured data.

- Service specifications and delivery notes serve to only as a supplement.

- The description must be specific enough to ensure that the project, location and scope of services can be clearly assigned.

This increases the structural recording effort. At the same time, it reduces the risk of invoices being deemed improper due to an inadequate description of services and thus jeopardising input tax deduction.

6 Changes in performance and their effects on the description

If the scope or content of the service changes - for example, due to relevant changes to the measurements for a construction service - the BMF considers this to be No mere change in the assessment basis, but a case for the Invoice correction at least with regard to the service description.

The management allows this correction - with corresponding prior agreement - to also be in the form of an (electronic) credit amount by the beneficiary is issued. This credit note must then refer to the original invoice in a specific and unambiguous manner.

This means for the service description:

- If the content of the service changes, this change must also be reflected in the structured part of the new or corrected e-bill.

- Annexes can explain the change, but do not replace the adaptation of the core description.

7. summary: guidelines for a clean service description

The specifications for the service description in the e-bill can be summarised in a few guiding principles:

- Mandatory information in the structured part: The service description must be included in the structured data of the e-bill.

- Control function in view: The type, scope and location of the service must be described in such a way that the tax authorities and recipient can clearly and easily allocate the service.

- Concise core, detailed appendix: A compact but clear description in the data core is possible; details may be added as an appendix.

- No links to the outside: References to external documents or links are not sufficient. All relevant information must be supplied with the e-bill.

- Make performance changes visible: If the service content changes, a corrected service description is required - either in a new invoice or in a credit note.

Those who take these guidelines into account in their invoicing processes utilise the scope of the e-invoice, simultaneously fulfil the formal requirements of the Federal Ministry of Finance and reduce the risk of later discussions about input tax deduction or the correctness of the invoice.

E-Invoicing 2026: What is changing now for SMEs and SAP B1 users

E-Invoicing 2026: From Receipt to Mandatory Issuance — what SMEs must clarify now

E-invoicing in Europe: Harmonised standard and national fragmentation

E-invoicing in SMEs: The clock is ticking

France E-invoicing 2026: What companies with a French tax number need to know now

Service description in the e-invoice: How much detail really needs to be included?

Verifactu in Spain: the new invoicing obligation

The e-invoicing regulations in Europe

The advantages of the e-bill 2025