The basic topic of mandatory e-invoicing has now arrived in most companies. The real uncertainty today lies elsewhere: in detailed questions, special cases and the differentiation between e-invoicing and other invoice types. This is precisely where the BMF letter dated 15 October 2025 (III C 2 - S 7287-a/00019/007/243) an.

This letter contains important adjustments and clarifications - including on Obligation to send e-invoices by small businesses and to the Differentiation between e-invoices and other invoices. The following seven facts will help you to categorise the existing rules correctly and avoid typical misinterpretations.

1. your PDF invoice is still not an e-invoice

One of the most persistent misconceptions remains: A PDF invoice sent by e-mail is not an e-invoice. Although it appears digital, it does not fulfil the requirements of a structured electronic invoice.

An e-bill must be issued in a structured electronic format be issued, transmitted and received, which Electronic processing is possible. These include formats that comply with the European standard EN 16931 correspond (like XInvoice or ZUGFeRD), or bilateral formats, provided that all required data can be correctly and completely extracted into an EN-16931-compliant format.

A simple PDF file or an image file is therefore legally considered a „other invoice“. Although it complies with formal invoice requirements, it does not fulfil the special requirements for a B2B e-invoice.

The new BMF circular dated 15 October 2025 picks up right here. It sharpens the Differentiation between e-invoices and other invoices once again and makes it clear that companies must consciously choose their formats and clearly classify them internally. In everyday life, this means that the familiar „Word-to-PDF“ workflow is no longer suitable for structured documents. B2B-processes are no longer a viable option.

2. a „broken“ e-invoice still remains an invoice

Technical errors in e-invoices cannot be completely avoided despite good preparation. It is therefore crucial how the BMF deals with faulty files.

According to the previous BMF margin notes, an e-invoice with Format errors is not simply „destroyed“. Instead, it becomes „other invoice in another electronic format“ downgraded. Although it loses its status as an e-invoice, it remains an invoice document.

This is practical because it prevents the immediate loss of a valid document in the event of technical faults. At the same time, this fallback rule has an important limit: the Direct validity for input tax deduction may be limited. Therefore, such an invoice should be issued by the issuer formally corrected become.

In conjunction with the BMF letter of 15 October 2025, it becomes clearer how important the dividing line between E-bill and Other invoice is. Companies should therefore introduce technical checking routines and at the same time maintain clear processes for corrections.

3. the obligation affects almost everyone - and the focus is on the recipient side

The original regulations make it clear how far-reaching the B2B e-invoicing obligation is: it applies to domestic transactions between companies based in Germany. This also includes Small businesses, farmers and foresters or entrepreneurs with only tax-free sales, such as landlords. Invoices to these groups must always be issued as e-invoices.

However, the real surprise has been on the recipient side since the beginning. The VAT application decree makes it clear: Every domestic entrepreneur, expressly including small businesses, must create the technical requirements to be able to receive e-invoices. „I can't receive“ is therefore no longer a viable argument.

The BMF letter dated 15 October 2025 picks up on this discussion when it Obligation to send e-invoices by small businesses addressed. At this point, it brings clarity to a topic that has often caused confusion in practice. Entrepreneurs should carefully analyse these clarifications and structure their communication and contractual relationships - especially with small businesses - accordingly.

4. there are still important exceptions to the e-invoicing obligation

Despite the far-reaching application of the E-invoicing obligationt exist some Clearly defined exceptions, that make a big difference in day-to-day business. According to the previous regulations, the following documents not be issued as an e-invoice:

- Invoices for small amounts whose total amount does not exceed 250 euros

- Tickets, for example train or flight tickets

- Invoices that of small entrepreneurs be issued

These exceptions are practical because they exempt everyday and frequent transactions from the more complex e-invoicing obligation. At the same time, companies must not overstretch them. Processes should be clearly documented, especially for mixed transactions and regularly recurring small amounts.

The BMF letter of 15 October 2025 does not change the fundamental existence of these exemptions. However, it emphasises the importance of a clean Differentiation of the various invoice types is. This increases the importance of clear internal guidelines for the question of when which form of invoice is permissible.

5. validation software is helpful - but not a free pass

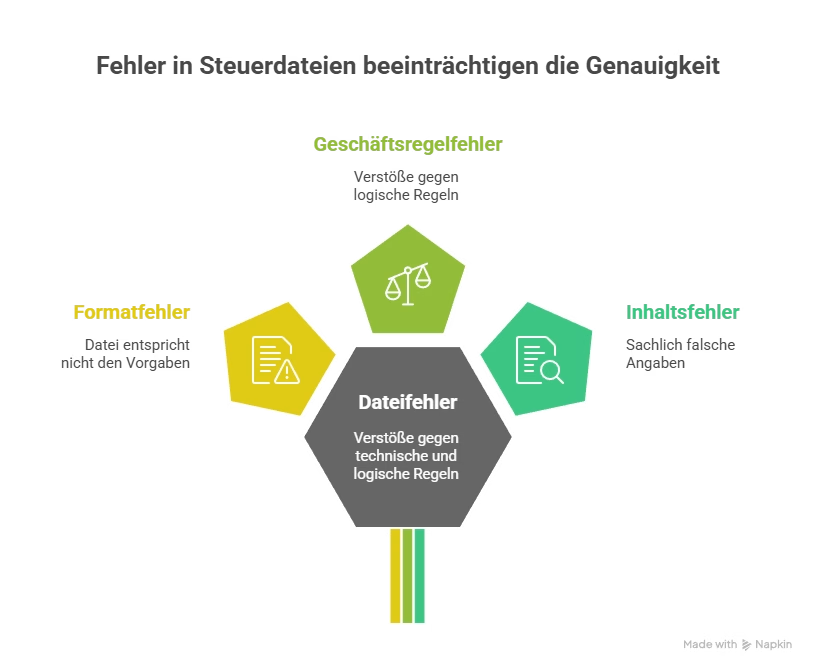

Many companies rely on special invoices for e-invoices. Validation software. These tools check whether a file fulfils the technical requirements. However, a „green tick“ from the software is not enough to ensure complete security.

The BMF distinguishes between three Error types:

- Format error - the file does not correspond to the technical specifications (e.g. incorrect XML structure).

- Business rule errors - the file violates logical rules (e.g. mathematical inconsistencies between tax amount and tax rate).

- Content error - the information is factually incorrect (e.g. incorrect tax rate, although the calculation is formally correct).

The central message of the BMF margin figures is: Validation does not replace the recipient's obligation to pay the invoice Content to check. Software reduces the risk of errors, but it is no substitute for commercial diligence.

Even in light of the new clarifications of 15 October 2025, this point remains unchanged: Companies need both technical as well as professional checking processes if you want to process e-invoices in a legally compliant manner.

6 The recipient is responsible - excuses no longer work

It used to be relatively easy for an invoice recipient to insist on a paper invoice. Those days are over. The new regulations clearly shift the responsibility to the Receiver side.

The Value Added Tax Application Decree states very clearly: An entrepreneur must No right to an alternative invoice (e.g. paper or simple PDF) simply because they are not technically able to receive an e-invoice. The issuer is deemed to have fulfilled its obligation if it has issued a correct e-invoice and has demonstrably endeavoured to transmit it.

In practice, this means

- Companies need to clarify proactively, like they receive e-invoices.

- You should define, via which channels (e.g. certain formats, portals or service providers).

- They must also ensure that this data into the accounting imports can be realised.

The BMF letter of 15 October 2025 addresses this issue by specifying the obligations to send and receive invoices - particularly with regard to small businesses and different types of invoices. This makes it even clearer that the responsibility does not lie solely with the issuer.

7 Unexpected leeway for archiving - but only for VAT

In many companies, the archiving of digital receipts is associated with the strict requirements of the GoBD. This is why one passage from the existing BMF margin notes on e-invoicing is particularly surprising.

It is clarified there that solely for the purposes of value added tax the Storage and archiving of e-invoices outside of a GoBD-compliant system does not automatically constitute an offence. This initially creates a certain amount of room for manoeuvre, particularly for transitional phases or simple structures.

However, the decisive note follows immediately: For other tax purposes, such as the Income or Corporate income tax, the strict GoBD rules continue to apply in full. So anyone who derives overly generous archiving rules on the basis of this one passage risks errors with other types of tax.

The new BMF circular dated 15 October 2025 does not change this principle, but it does sharpen the Differentiation of invoice types and thus indirectly also the question of which documents should be stored and how. Companies should therefore always adapt their archiving strategy overall tax not only with regard to VAT.

E-Invoicing 2026: What is changing now for SMEs and SAP B1 users

E-Invoicing 2026: From Receipt to Mandatory Issuance — what SMEs must clarify now

E-invoicing in Europe: Harmonised standard and national fragmentation

E-invoicing in SMEs: The clock is ticking

France E-invoicing 2026: What companies with a French tax number need to know now

Service description in the e-invoice: How much detail really needs to be included?

Verifactu in Spain: the new invoicing obligation

The e-invoicing regulations in Europe

The advantages of the e-bill 2025